Impact Update: Market Headwinds and Zombie Inflation

The first quarter of 2024 started with a bang! The S&P 500 ended March up about 11%. In April, the market gave back almost half of the gains, and is now up around 6% for the year. Almost every other asset class has lagged behind, with the notable bright spot being Gold, which has returned 15% year-to-date.

Domestic large caps led the rally, with NVIDIA at the forefront, driven by the boom in artificial intelligence which had lifted the US indices to new highs. AI seems to be more than just hype at this point, as the demand for graphics processing units has been catapulting NVIDIA and other AI companies much higher.

We also saw a huge run in cryptocurrency, led by Bitcoin, which has rallied as high as $70k. This marks a massive increase since it had retreated to $16k a little over two years ago.

The market rally broadened out to include international stocks and small caps, which largely lagged the market last year. Although, during the recent pullback over the past three weeks, we have seen some of these returns evaporate.

Zombie Inflation

ILLUSTRATION: IMAGE TEN, INC.

What is driving the recent market downturn? There are two main themes causing market volatility this year. The first is worries about an all-out war between Iran and Israel in the Middle East. Fortunately, it seems that this has been contained for the time being.

The second challenge is that inflation and interest rates are still stubbornly high at this point. It's kind of like a scene from a horror movie where the zombie rises again just when you think it's been defeated.

The year started with the market pricing in five rate cuts by the Federal Reserve. Just when we thought we were out of the woods, the last three inflation reports have come in higher than expected, with inflation running at 3.5% year over year. The Federal Reserve has a dual mandate of keeping both unemployment and inflation low, with the inflation target being 2%.

Why is inflation so persistent? Well, the economy is actually performing really well by any traditional measure. The unemployment rate is at a 50-year historical low of 3.8%, while the gross domestic product is expanding. It’s extremely hard to have an economy firing on all cylinders and at the same time keep inflation low.

Difficult Bond Market

Thanks to inflation, the 10-year treasury, which helps set interest rates on mortgages, credit cards, and car loans, has spiked higher. The 10-year treasury, which started the year off at 3.9%, has now increased to 4.6%. This may not sound like much, but this is an 18% increase in a short period of time.

This has put some major downward pressure on fixed income, real estate, and clean energy companies.

The Barclays Bond Aggregate is now down 3% year-to-date. The bond sell off has hurt more conservative investment portfolios that have a heavier weighting towards bonds.

The past few years have been extremely tough for the bond market. The Barclays U.S. Aggregate Bond Index has only been negative five times since 1976, with two of the five years being 2021 and 2022.

Does it still make sense to own bonds? Absolutely. Bonds can play a critical role in an investment strategy by reducing overall volatility in a portfolio. The reason is that if we have a major downturn or recession, then you'd expect the Federal Reserve to slash interest rates, which will cause the price of existing bonds to rise in value effectively creating a buffer or hedge.

Unlike 2021 and 2022 when interest rates were close to zero, the Fed Funds rate is now at 5.25% so there is a lot of upside potential if or when the Fed starts to cut rates.

Sustainable Investing

Unfortunately, the clean energy sector is very sensitive to higher interest rates. The IEA (International Energy Agency) has stated that just a 5% increase in interest rates makes the cost of solar and wind energy 33% more expensive.

At Impact Fiduciary, we target about 10% of the equity portfolio in clean energy while divesting from fossil fuel energy companies. This is an area that has been a drag on performance year-to-date.

At the same time, clean energy is actually fairly inexpensive when looking at the growth rate and valuations. This is an area that should perform very well when rates eventually drop or stabilize.

I view clean energy as a win-win scenario, with companies in this space offering not only high potential returns, but also the best chance for humanity to avert a climate catastrophe.

Real Estate Investment Trusts (REITS)

Rising interest rates are not very friendly to the real estate sector. Real estate investment trusts or REITs are now down about 7% year-to-date. REITs are considered an alternative asset class that are non-correlated to stocks and bonds. They provide an additional layer of diversification and have averaged around 12% annually over the past fifty years so there is a considerable amount of upside potential.

One misnomer that I hear quite bit is that publicly traded REITs only invest in commercial office space and shopping malls. The reality is that they are extremely well diversified and represent over $1.75 trillion in real assets!

Here is a breakdown of the current mix of Impact’s real estate exposure which spans across hospitals, residential holdings, nursing homes, storage facilities, and even data storage systems.

Snapshot of the Dimensional Fund Global Real Estate Allocation (DFGR)

Where do we go from here?

My view is that trying to act on short-term predictions is a fool's errand. What we will do in a choppy market environment is look for opportunities to rebalance the portfolio and take advantage of tax loss harvesting in taxable investment accounts.

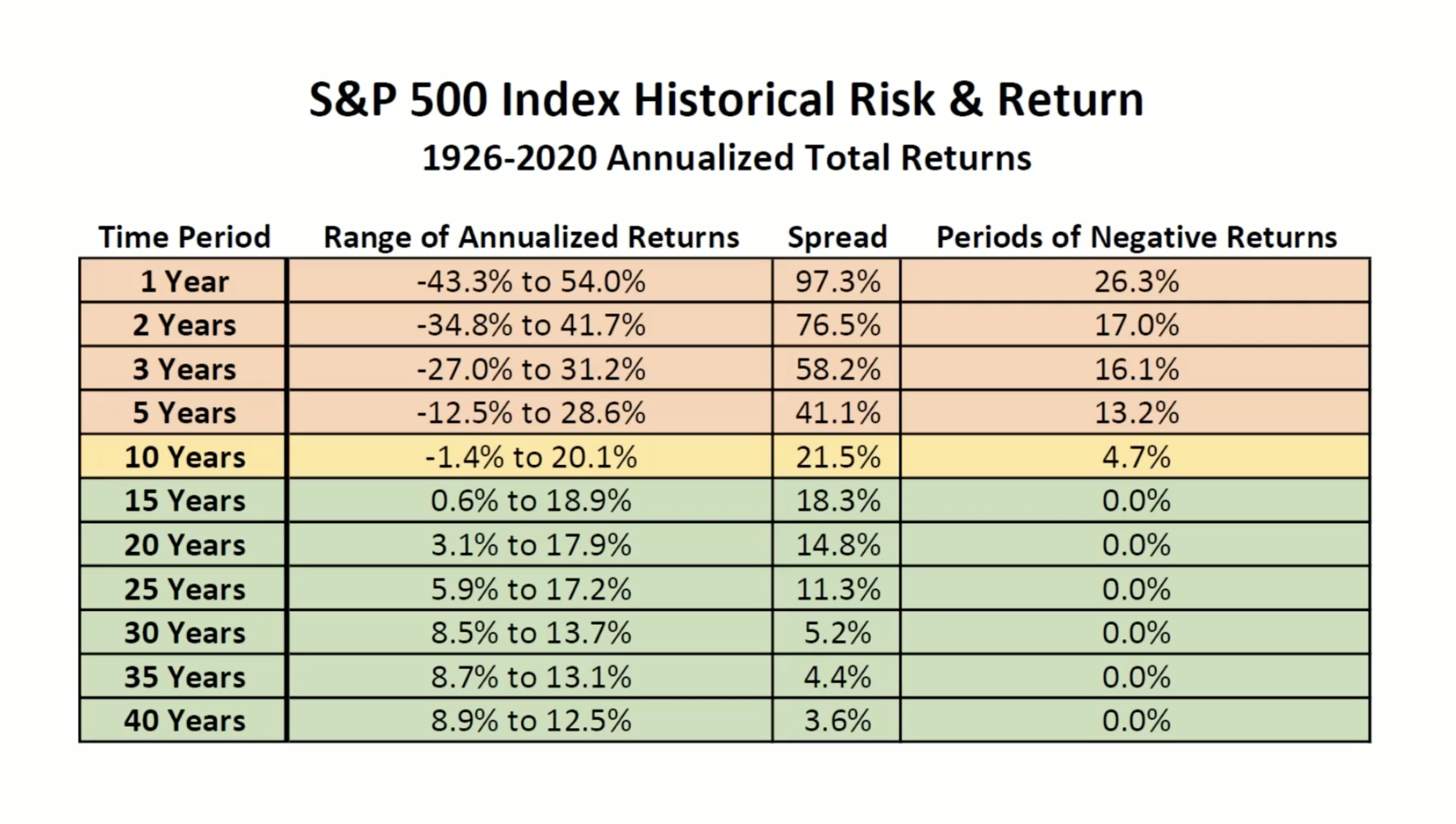

Successful investing in the market is 100% about diversification and having the right time horizon. Even over a period of a few years, you can have negative returns if you only invest in a single slice of the market like the S&P 500 or just have unlucky timing.

As you can see in the chart to the right labeled, S&P 500 Historical Risk & Return, the odds grow increasingly in your favor as you have more time to stay invested.

I’ve found that the recipe for success is to simply automate investing your excess savings so that you only have to make one upfront decision instead of many. This will help you “buy the dip” and smooth out returns over time.

If you are investing, then you should expect to have a correction, which is defined as a 10% pullback, about once every 18 months. Corrections and bear markets can be painful, but market volatility is the price of admission when it comes to realizing higher returns over the long-term.

My best recommendation is to hold your nose in difficult periods and put the cash to work. Your future self will thank you for it!

In the spirit of Earth Month, I’ll leave you with a great quote that I recently came across from Thích Nhất Hạnh.

“People usually consider walking on water or in thin air a miracle. But I think the real miracle is not to walk either on water or in thin air, but to walk on earth. Every day we are engaged in a miracle which we don’t even recognize: a blue sky, white clouds, green leaves, the black, curious eyes of a child—our own two eyes. All is a miracle.”

Disclaimer: This article is provided for general information and illustration purposes only. Nothing contained in the material constitutes tax advice, a recommendation for purchase or sale of any security, or investment advisory services. I encourage you to consult a financial planner, accountant, and/or legal counsel for advice specific to your situation. Reproduction of this material is prohibited without written permission from Patrick Dinan, and all rights are reserved.